CRE Debt - Sizing Constraints

Got Debt?

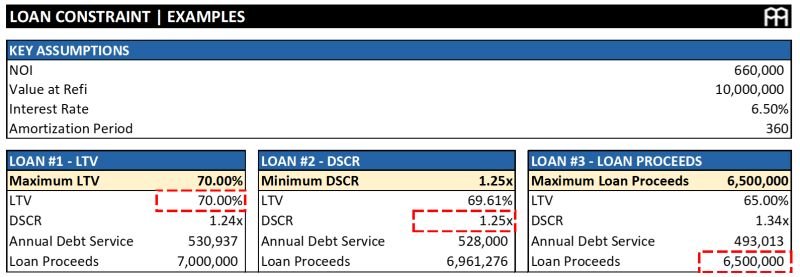

When determining how much debt to deploy, lenders rely on a few key constraints, including: 1) Loan-to-Value (LTV), 2) Minimum Debt Service Coverage Ratio (DSCR), and 3) Maximum Loan Proceeds.

The below example and chart illustrate how LTV, Minimum DSCR, and Maximum Loan Proceeds impact the following investor scenario: An investor owns an asset producing $660K of net operating income (NOI) annually, valued at $10MM using a 6.6% cap rate (Cap Rate=NOI/Asset Value).

Loan #1 - LTV: Loan-to-Value (LTV) is the ratio of the loan amount to the property’s value, and is typically capped to limit lender risk. In this case, the lender limited the loan to 70% of the property’s value, restricting loan proceeds to $7,000,000.

Loan #2 - DSCR: The DSCR measures an asset's ability to cover debt payments with cash flow. Here, the lender requires a minimum DSCR of 1.25x, meaning the NOI of $660K must be 25% greater than the debt service, capping annual debt service at $528K ($660K÷1.25). Using this maximum debt service, we can calculate the maximum allowable loan proceeds of $6,961,276.

Loan #3 - Loan Proceeds: Here, the loan is constrained by the lender’s maximum loan proceeds limit. Although the borrower’s LTV & DSCR support a higher loan amount, the loan is capped at $6,500,000.